PROXY MONITOR

REPORT

Fall 2013

Corporate Governance and Shareholder Activism

By James R. Copland and Margaret M. O’Keefe

DOWNLOAD PDF

In recent years, large, publicly traded American corporations have increasingly faced pressure from a subset of shareholder activists that introduce proposals on the companies’ proxy ballots for consideration at annual meetings. This report draws upon information in the Proxy Monitor database to assess the 2013 proxy season in historic context. Among its key findings:

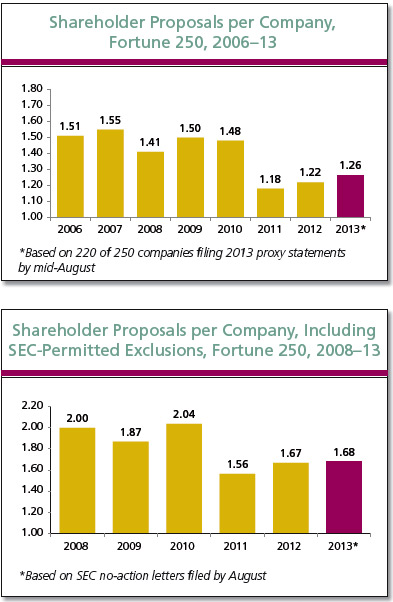

- The number of shareholder proposals introduced is up. The average Fortune 250 company faced 1.26 shareholder proposals on its 2013 proxy statement, up slightly from 1.22 proposals per company in 2012. This trend also holds when considering the 104 proposals excluded from proxy ballots after companies received a letter from the Securities and Exchange Commission assuring them that the agency would take no action against the company due to the proposal’s procedural or substantive defects.

- Support for shareholder proposals is down. Only 7 percent of shareholder proposals received the backing of a majority of shareholders in 2013, down from 9 percent in 2012. A smaller percentage of shareholder proposals passed in 2013 than in any other year in the 2006–13 period. Among the 20 proposals receiving majority support, 13 involved just two issues: whether to elect all corporate directors annually and whether each director should be required to receive a majority of votes cast to be elected.

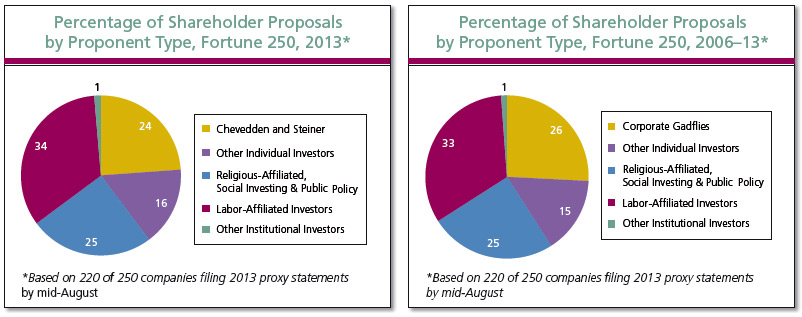

- The overwhelming majority of shareholder proposals are sponsored by a small subset of shareholders. In both 2013 and the full 2006–13 period, only 1 percent of shareholder proposals were sponsored by institutional investors unaffiliated with organized labor or a social, religious, or public-policy purpose. A plurality of all proposals, 34 percent, were sponsored by labor-affiliated investors, primarily pension funds for private- or public-sector workers. Twenty-five percent were sponsored by social or policy investors, chiefly “social investing” funds and pension funds or other investment vehicles affiliated with religious institutions. Twenty-four percent were sponsored by just two individuals, John Chevedden and Kenneth Steiner, and their family members and trusts.

- The most frequent sponsors of shareholder proposals, labor-union pension funds, could be targeting companies for reasons other than shareholder value, including the companies’ political participation. Among the 41 Fortune 250 companies contributing $1.5 million or more to the political process in the 2012 election cycle, 44 percent faced a labor-sponsored proposal, as opposed to only 18 percent of all other companies. Those companies that gave at least half of their donations to support Republicans were more than twice as likely to be targeted by shareholder proposals sponsored by labor-affiliated funds as those companies that gave a majority of their politics-related contributions on behalf of Democrats.

- Shareholder proposals related to corporations’ political spending or lobbying constituted a plurality of all proposals in 2013 but continued to attract little support. As in 2012, 82 percent of shareholders opposed proposals related to political spending or lobbying in 2013. Moreover, controlling for proposal class, support for these proposals fell in 2013: Shareholder support for lobbying-related proposals fell from 22 percent to 20 percent, year over year, and support for proposals relating exclusively to political spending fell from 17 percent to 16 percent. Overall support remained flat because the share of proposals related to lobbying jumped from 33 percent to 54 percent, most likely because 2013, unlike 2012, is not a federal election year.

Consistent with the conclusion of the 2012 Proxy Monitor report and other empirical analyses conducted over the past three years, results from the 2013 proxy season suggest that the shareholder-proposal process may not be serving the ordinary investor’s interests. A small subset of investors continues to dominate this process, and the most active of those, labor-affiliated pension funds, could be motivated by political concerns. The evidence suggests that the shareholder-proposal process, as currently organized, may be facilitating a transfer of wealth from the average diversified investor to a subset of investors interested in goals other than share value—and inconsistent with efficiency, competition, and capital formation.

|

ABOUT PROXY MONITOR

|

The Manhattan Institute’s ProxyMonitor.org database, launched in 2011, is the first publicly available database cataloging shareholder proposals[1] and

Dodd-Frankmandated executive-compensation advisory votes[2] at America’s largest companies.[3] This is the third annual survey and 22nd

publication in a series of findings and reports by Manhattan Institute Center for Legal Policy director James R. Copland, each drawing upon information in the database to examine

shareholder activism in which investors attempt to influence corporate management through the shareholder voting process.[4]

|

In 2013, America’s largest publicly traded companies faced an increased level of shareholder activism in the form of shareholder proposals, which can be introduced on corporate proxy statements by any owner of the company’s equity securities valued at $2,000 or more and held for the preceding year.[5] As has been the case in recent years,[6] these proposals were generally introduced by a small subset of shareholders and focused on corporate-governance concerns (i.e., rearranging the rules aligning power between shareholders and directors), executive-pay practices, and social or policy goals. As in 2012, the most frequently introduced classes of proposals involved corporate political spending or lobbying and separating the positions of chairman and chief executive officer—the latter most prominently in an unsuccessful push led by labor-union pension funds to split the chairman and CEO roles at JPMorgan Chase.[7] Corporate-governance issues gained increased attention in the broader public consciousness in July, when former New York attorney general Eliot Spitzer declared his candidacy for New York City comptroller, explicitly promising to leverage New York’s pension-fund assets to reshape corporate America.[8]

This report examines 2013 trends in shareholder-proposal activism in historic context. Data in the report are drawn from the Manhattan Institute’s publicly available database, ProxyMonitor.org, which collates the Fortune 250 companies’ public proxy filings with the Securities and Exchange Commission (SEC), dating back to 2006. Data for 2013 are current to August 15, at which time 220 of the Fortune 250 companies had filed proxy documents with the SEC and 218 had held their annual meetings.

This report examines 2013 trends in shareholder-proposal activism in historic context. Data in the report are drawn from the Manhattan Institute’s publicly available database, ProxyMonitor.org, which collates the Fortune 250 companies’ public proxy filings with the Securities and Exchange Commission (SEC), dating back to 2006. Data for 2013 are current to August 15, at which time 220 of the Fortune 250 companies had filed proxy documents with the SEC and 218 had held their annual meetings.

Part I of this report gives an overview of shareholder proposals introduced in 2013, not only including proposals making the proxy ballot but also giving special focus to those proposals that were introduced by shareholders but that companies excluded from the ballot after receiving a letter from the SEC permitting them to do so. Part II looks at who was driving shareholder-proposal activism in 2013, with a special focus on the efforts of labor-affiliated investors, which disproportionately targeted companies active in the political process, especially those companies that gave more heavily in support of Republicans. Part III looks at the subject matter of shareholder-proposal activism in 2013, with a special focus on those related to corporate political spending or lobbying, which constituted a plurality of all shareholder proposals but gained little support in shareholder votes. Part IV looks more broadly at voting results for shareholder proposals in 2013, as well as for executive compensation advisory votes.

I. Shareholder-Proposal Incidence in 2013

In 2013, the average Fortune 250 company faced 1.26 shareholder proposals on its proxy statement, up slightly from 1.22 proposals per company in 2012. The number of shareholder proposals faced per company remains below the level witnessed before 2011—a trend significantly explained by the 2010 passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act,[9] which required regular shareholder advisory votes on executive compensation beginning in 2011,[10] thus obviating the need for one of the shareholder proposals most regularly introduced in earlier years.

The shareholder proposals listed on corporate ballots present only a partial picture of shareholder-proposal activity because many shareholder proposals that are introduced never make it onto a proxy ballot. In some instances, the company receiving the shareholder proposal negotiates with the proposal sponsors to withdraw the proposal. In other cases, the company excludes the ballot item without the consent of the sponsor—almost always after receiving a formal letter from the SEC stating that the agency will not pursue legal action against the company for doing so.[11] Including the proposals in which companies have received a formal “no-action” letter from the SEC after petitioning the agency seeking to exclude a shareholder-proposed ballot item (see “Special Focus: Proposals Excluded from Proxies with SEC Permission”),[12] Fortune 250 companies faced 1.68 shareholder proposals on average in 2013—also up marginally from 2011 and 2012 but below the level witnessed before Dodd-Frank.[13]

|

SPECIAL FOCUS: PROPOSALS EXCLUDED FROM PROXIES WITH SEC PERMISSION

|

Under SEC regulations governing shareholder proposals,[14] a publicly traded company may exclude a shareholder proposal from its proxy ballot under certain conditions. Such reasons can include procedural defects (e.g., missing a deadline or failing to establish actual or adequate stock ownership in the company), in addition to various substantive reasons (e.g., the proposal conflicts with state law, it duplicates or conflicts with another proposal on the ballot, it involves the “ordinary business operations” of the company, it is too vague or indefinite, or the company has already substantially implemented the proposal or lacks the power to implement it).[15] A company wishing to exclude a shareholder proposal from its proxy will typically seek a formal letter from the SEC permitting it to do so, based on one of these rationales.

Under SEC regulations governing shareholder proposals,[14] a publicly traded company may exclude a shareholder proposal from its proxy ballot under certain conditions. Such reasons can include procedural defects (e.g., missing a deadline or failing to establish actual or adequate stock ownership in the company), in addition to various substantive reasons (e.g., the proposal conflicts with state law, it duplicates or conflicts with another proposal on the ballot, it involves the “ordinary business operations” of the company, it is too vague or indefinite, or the company has already substantially implemented the proposal or lacks the power to implement it).[15] A company wishing to exclude a shareholder proposal from its proxy will typically seek a formal letter from the SEC permitting it to do so, based on one of these rationales.

In 2013, a plurality of the 104 formal no-action letters written by the SEC to Fortune 250 companies in response to a corporate petition cited procedural defects as a reason permitting the company to exclude a shareholder proposal. The agency’s second-most cited rationale permitting exclusion was that the proposal was too “vague and indefinite.”

As one might expect, individual investors’ shareholder proposals are far more likely to generate a successful SEC no-action petition than those of institutional investors. In 2013, 86 percent of proposals excluded from proxy ballots after an SEC no-action letter were sponsored by individual investors, as opposed to 8 percent by labor-affiliated institutional investors (chiefly funds for workers’ pension benefits) and 6 percent by institutional investors with a social, religious, or public-policy focus. No institutional investor without a labor affiliation or a social, religious, or policy focus introduced a shareholder proposal that generated a successful no-action petition to the SEC last year.

|

II. Sponsors of Shareholder Proposals in 2013

As has been the case every year in the ProxyMonitor.org database, dating back to 2006, a small number of shareholders dominated the shareholder-proposal process in 2013, and there was virtually no involvement on the part of institutional investors without a tie to organized labor or a social, religious, or public-policy purpose. A plurality of all shareholder proposals that appeared on proxy ballots (34 percent) were sponsored by labor-affiliated institutional investors in 2013, up slightly from the full 2006–13 period (33 percent). These investors are primarily employee pension funds, both for private-sector union members and for state and municipal employees (see “Special Focus: Labor-Affiliated Pension Funds”)—chiefly, in 2013, the American Federation of Labor–Congress of Industrial Organizations (AFL-CIO); the American Federation of State, County, and Municipal Employees (AFSCME); the International Brotherhood of Electrical Workers; and the pension funds for the employees of New York City and State. Some 25 percent of all shareholder proposals were sponsored by institutional investors with a social, religious, or public-policy purpose in 2013, an identical percentage to that in the full 2006–13 period. These investors are primarily “social investing” funds with an express purpose beyond mere share-price maximization (most commonly, Trillium Asset Management) and pension funds or other investment vehicles managed by churches or other religious organizations (most commonly, Catholic orders of nuns or monks). In keeping with the full 2006–13 period, only 1 percent of all shareholder proposals were sponsored by other institutional investors.

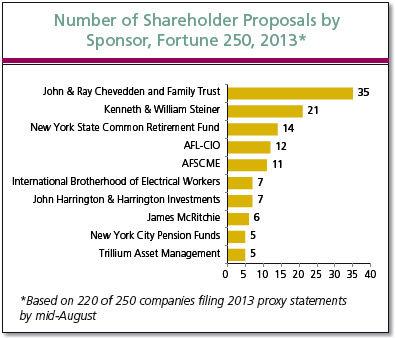

Individual investors sponsored 40 percent of all shareholder proposals in 2013, down slightly from 41 percent in the full 2006–13 period. 60 percent of these individual-backed proposals were sponsored by just two individuals and their family members and family trusts: John Chevedden and Kenneth Steiner.[16] These individuals, who repeatedly file common proposals at multiple companies, are commonly called “corporate gadflies.”[17] Chevedden and Steiner alone sponsored almost as large a percentage of shareholder proposals in 2013 (24 percent) as the four most common gadflies did across the full 2006–13 period (26 percent). (Two of the four most common gadflies over the 2006–13 period, Evelyn Davis and Emil Rossi, were inactive this year.) The role played by Chevedden and Steiner is understated by looking at proxy-ballot submissions alone: of the 104 shareholder proposals excluded from proxy ballots after the company successfully petitioned the SEC for a no-action letter, 23 had been filed by Chevedden and seven by Steiner. Among the shareholder proposals sponsored by individuals other than Chevedden and Steiner, 38 percent were filed by just three individuals: James McRitchie and Gerald Armstrong, who are also shareholder activists in the “gadfly” mold; and John Harrington, a social investor who also files proposals through his social-investing fund Harrington Investments.

Individual investors sponsored 40 percent of all shareholder proposals in 2013, down slightly from 41 percent in the full 2006–13 period. 60 percent of these individual-backed proposals were sponsored by just two individuals and their family members and family trusts: John Chevedden and Kenneth Steiner.[16] These individuals, who repeatedly file common proposals at multiple companies, are commonly called “corporate gadflies.”[17] Chevedden and Steiner alone sponsored almost as large a percentage of shareholder proposals in 2013 (24 percent) as the four most common gadflies did across the full 2006–13 period (26 percent). (Two of the four most common gadflies over the 2006–13 period, Evelyn Davis and Emil Rossi, were inactive this year.) The role played by Chevedden and Steiner is understated by looking at proxy-ballot submissions alone: of the 104 shareholder proposals excluded from proxy ballots after the company successfully petitioned the SEC for a no-action letter, 23 had been filed by Chevedden and seven by Steiner. Among the shareholder proposals sponsored by individuals other than Chevedden and Steiner, 38 percent were filed by just three individuals: James McRitchie and Gerald Armstrong, who are also shareholder activists in the “gadfly” mold; and John Harrington, a social investor who also files proposals through his social-investing fund Harrington Investments.

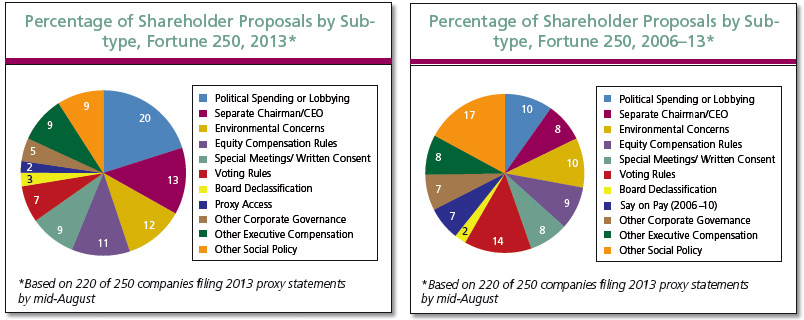

III. Subject Matter of 2013 Shareholder Proposals

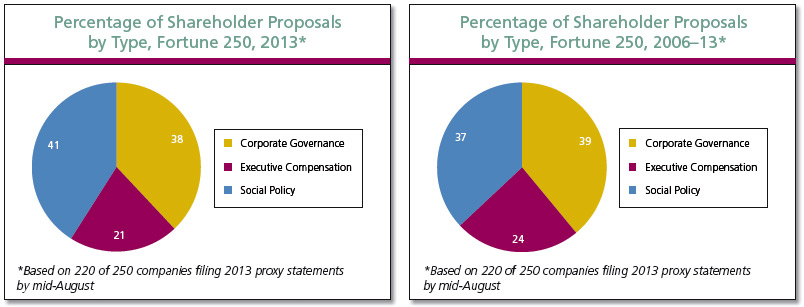

In 2013, shareholder proposals related to social or policy issues such as political spending, the environment, or human rights constituted a greater percentage of all shareholder proposals (41 percent) than the norm over the full 2006–13 period (37 percent). Conversely, the 2013 share of proposals related to corporate governance, such as de-staggering the board of directors (to elect each director annually), requiring directors to receive a majority of the vote for election (as opposed to a plurality), or separating the company’s chairman and CEO positions fell one percentage point below the eight-year average (38 percent, as opposed to 39 percent). The fraction of shareholder proposals related to executive compensation was three percentage points below that in the full 2006–13 period (21 percent, as opposed to 24 percent).

|

SPECIAL FOCUS: LABOR-AFFILIATED PENSION FUNDS

|

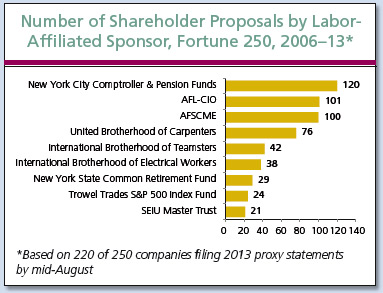

In 2013, as throughout the 2006-13 period, the most active sponsors of shareholder proposals on corporate proxy ballots have been institutional investors affiliated with organized labor, typically pension funds for state or municipal employees (such as the New York State Common Retirement Fund), pension funds affiliated with private-sector labor unions (such as the AFL-CIO), or pension funds affiliated with public workers but not through a state- or local-backed plan (such as AFSCME). Although the New York State Common Retirement Fund was the most active institutional investor in sponsoring shareholder proposals in 2013 (introducing 14 proposals), its aggressive activism is relatively recent. Over the full 2006–13 period, the most active institutional investors in the shareholder-proposal process were the New York City pension funds and comptroller’s office.[18]

In 2013, as throughout the 2006-13 period, the most active sponsors of shareholder proposals on corporate proxy ballots have been institutional investors affiliated with organized labor, typically pension funds for state or municipal employees (such as the New York State Common Retirement Fund), pension funds affiliated with private-sector labor unions (such as the AFL-CIO), or pension funds affiliated with public workers but not through a state- or local-backed plan (such as AFSCME). Although the New York State Common Retirement Fund was the most active institutional investor in sponsoring shareholder proposals in 2013 (introducing 14 proposals), its aggressive activism is relatively recent. Over the full 2006–13 period, the most active institutional investors in the shareholder-proposal process were the New York City pension funds and comptroller’s office.[18]

Apart from the pension funds for New York City and State, state and municipal employee pension funds have played a relatively minor role in shareholder-proposal activism. Instead, most shareholder proposals backed by labor-affiliated investors have been sponsored by pension funds independent of states and municipalities, representing workers in both the private and public sectors. The most active of these have been the private-sector AFL-CIO and public-sector AFSCME, which have sponsored 101 and 100 shareholder proposals, respectively, at Fortune 250 companies dating back to 2006.

Behind the New York City pension fund, the AFL-CIO, and AFSCME, the fourth most active labor-affiliated sponsor of shareholder proposals dating back to 2006 is the United Brotherhood of Carpenters pension fund, with 76 proposals sponsored. The carpenters’ union has been far less active to date in 2013, sponsoring only two proposals, which may reflect a change in strategy related to the fund’s shareholder-activism efforts.

Behind the New York City pension fund, the AFL-CIO, and AFSCME, the fourth most active labor-affiliated sponsor of shareholder proposals dating back to 2006 is the United Brotherhood of Carpenters pension fund, with 76 proposals sponsored. The carpenters’ union has been far less active to date in 2013, sponsoring only two proposals, which may reflect a change in strategy related to the fund’s shareholder-activism efforts.

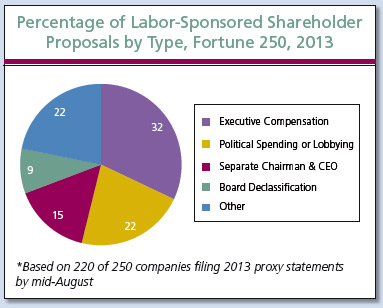

A plurality of all shareholder proposals backed by labor-affiliated funds in 2013 (32 percent) have related to executive compensation. Some 22 percent of proposals have related to corporate political spending or lobbying, and 15 percent have sought to separate the company’s chairman and CEO positions. Because executive pay is obviously sensitive for corporate management, as is a proposal seeking to separate the chairman and CEO roles in companies where such duties are assigned jointly—in effect, requiring CEOs to take a boss on the board of directors or give up day-to-day control of the company’s operations—“labor’s disproportionate role in backing this class of proposals raises the prospect that unions are attempting to leverage the shareholder-proposal process to gain negotiating position over management.”[19] In addition, the significant focus of some union pension funds on corporate political spending or lobbying and other social or policy issues “raises the question of whether these funds’ activism is intended to advance a political agenda for reasons other than increasing shareholder returns.”[20]

For state and municipal employee pension funds as well as private pension funds, the focus of shareholder activism has not been uniform. The New York funds have focused their shareholder activism overwhelmingly on social and public policy issues; but other state and municipal pension funds—in addition to being notably less active—have, for the most part, introduced shareholder proposals related to traditional corporate-governance questions, such as declassifying the board of directors (electing all directors annually) or requiring a simple majority vote to elect directors (rather than a plurality).[21] The United Brotherhood of Carpenters pension fund has a reputation for being rigorous and value-oriented in its approach to shareholder activism. It has earned this reputation because most of its proposals have sought a majority-voting standard for electing directors.[22]

Notwithstanding these caveats, earlier reports in the Proxy Monitor series have shown that labor-affiliated pension funds have tended to focus their shareholder-proposal activism on companies and sectors that seem to have little to do with share value but may be related to labor-organizing efforts or other labor disputes with company management, or otherwise with a political agenda.[23] Under the federal Employee Retirement Income Security Act (ERISA),[24] private employee fund managers are required to “consider only those factors that relate to the economic value of the plan’s investment” and cannot “subordinate the interests of the participants and beneficiaries in their retirement income to unrelated objectives.”[25] These legal strictures do not apply to state and municipal employee pension funds or to pension funds affiliated with a religious organization.[26]

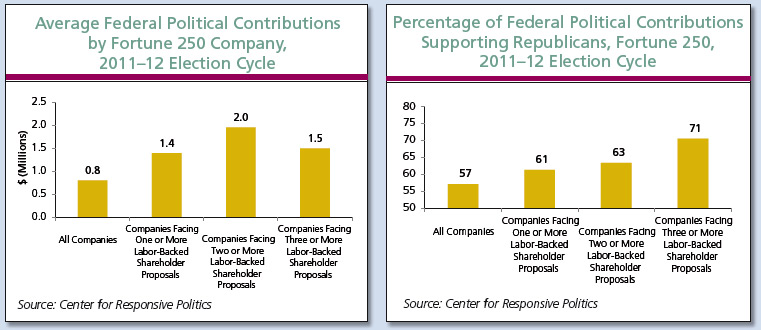

In 2013, the focus of labor-affiliated funds' shareholder-proposal activism again broadly supports the hypothesis that at least some of these funds' efforts in this area may have a political purpose. Campaign giving is the norm of the nation’s largest corporations: every one of the Fortune 250 American companies tracked by Proxy Monitor contributed some funds to the political process in the 2012 election cycle (through political action committees [PACs] or otherwise).[27] On average, each company and its PACs gave almost $800,000 to candidates or political committees.[28] Some companies, however, contributed significantly more to such groups, with 41 of the 250 companies giving at least $1.5 million.[29] Those companies, as a group, were much more likely to be targeted by shareholder proposals introduced by labor-affiliated pension funds in 2013: 44 percent of these politically most active companies faced a labor-sponsored proposal, as opposed to only 18 percent of all other companies. What’s more, those corporations that gave at least half of their donations to support Republicans were more than twice as likely to be targeted by shareholder proposals sponsored by labor-affiliated funds as those companies that gave a majority of their politics-related contributions on behalf of Democrats.

The average company targeted by labor-affiliated investors' shareholder proposals in 2013 had spent almost $1.4 million on the political process in 2012, almost 75 percent higher than the average company overall. The average company facing multiple labor-backed proposals spent almost $2 million, almost 145 percent above average. The share of 2012 Fortune 250 dollars going to back the GOP was 57 percent for all companies but 61 percent among companies facing a shareholder proposal with a labor-affiliated sponsor in 2013. Companies facing two or more labor-backed shareholder proposals had allocated 63 percent of their political dollars to help Republicans, and the five companies that faced at least three shareholder proposals sponsored by labor-affiliated funds gave 71percent of their political dollars to support the GOP.[30]

Those five companies facing three or more labor-sponsored shareholder proposals in 2013 were the health-care company Abbott Laboratories (ABT, five proposals); the telecommunications company CenturyLink (CTL, three proposals); milk-products producer and distributor Dean Foods (DF, three proposals); oil giant ExxonMobil (XOM, four proposals); and the mining company Freeport-McMoRan Copper & Gold (FCX, four proposals). Abbott, Dean, and ExxonMobil were also three of the four companies receiving three or more proposals in 2012,[31] and, as was the case last year, labor funds’ particular focus on these companies does not appear to be plausibly related to share value. Abbott’s shares returned 26.5 percent in the year preceding the February 27 record date for shareholders to vote at the 2013 annual meeting and 31.9 percent over the preceding three years. For both time spans, Abbott’s share returns were better than those for Merck and Johnson & Johnson, though behind those for Pfizer and Eli Lilly; but AbbVie, the patent pharmaceutical portfolio company that Abbott spun off in a one-toone share split in January 2013,[32] was up 30.5 percent by the 2013 record date, between 50 and 100 percent better than its four large domestic competitors. For the year preceding Dean’s March 23 record date, the company’s shares were up 49.8 percent, between 200 and 300 percent better than Kraft or General Mills. The company’s 14.8 percent three-year return trailed General Mills but outperformed both Kraft and its spin-off company, Mondelez International. ExxonMobil returned 5.6 percent and 31.7 percent over one- and three-year windows preceding its April 4 record date, trailing Chevron but besting BP, Royal Dutch Shell, Total, and ConocoPhillips among other large, non-stateowned petroleum companies in both periods.[33]

As suggested in last year's report, labor unions' focus on these three companies is at least plausibly due to factors other than share value. Abbott’s split into two companies might be viewed as portending staff streamlining, and “Abbott CEO Miles White very publicly supported controversial changes to laws governing public-employee unions in Wisconsin, Illinois, and other states.”[34] Dean Foods is going through a reorganization and consolidation plan that threatens to close 10–15 percent of the company’s facilities—endangering jobs at the company, which is roughly 40 percent unionized[35]—and “has been targeted by the California Farmers Union for exerting market pressure on dairy farmers.”[36] ExxonMobil’s PAC and affiliates contributed almost $2.8 million to the 2011–12 political cycle, with 89 percent of those donations going to Republican candidates and committees.[37]

The two “new” companies targeted by labor-affiliated funds in 2013, CenturyLink and Freeport-McMoRan, are plausibly under scrutiny due to share-price performance: CenturyLink missed profit and revenue expectations in February,[38] and its shares fell 9.4 percent and 2.3 percent in the one- and three year windows preceding the company’s April 4 record date, significantly behind the performance of competitors AT&T and Verizon;[39] and Freeport’s shares fell 6.7 percent and 49.2 percent over the one- and three-year windows preceding its May 24 record date—well back of international competitors BHP, Glencore Xstrata, and Grupo Mexico—in part due to a mine collapse in the company’s Indonesian Grasberg copper mines, the world’s second-largest.[40] The poor share-price performance of each company, however, is significantly attributable to laborcontract negotiating and unrest, which also offers an alternative hypothesis for the labor-affiliated funds’ focus. CenturyLink was actively involved in labor negotiations with the Communications Workers of America (CWA), which just reached a new four-year labor agreement with the company this summer.[41] (The CWA, International Brotherhood of Electrical Workers, and pension fund for U.S. West retirees were, along with the New York State Common Retirement Fund, the labor-affiliated pension funds sponsoring shareholder proposals with CenturyLink in 2013.) As of this writing, Freeport-McMoRan has yet to resolve labor negotiations with the government of Indonesia, where the company’s existing labor contract is set to expire in September.[42] The company’s workers threatened to strike this summer, the business is still recovering from a three month strike in late 2011, and Indonesia is holding elections in 2014.[43] Freeport faced 2013 proposals from the New York State and City pension funds and the California State Teachers Retirement System (CalSTRS), as well as AFSCME.

|

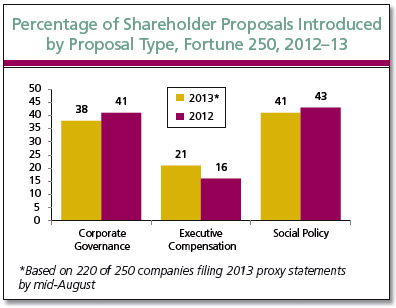

Relative to 2012, however, the percentage of shareholder proposals related to executive compensation rose by five percentage points, from 16 percent to 21 percent, and the share of corporate-governance and social-policy proposals likewise fell. From 2006 through 2010, 27 percent of all shareholder proposals related to executive compensation, but more than one-third of these proposals sought shareholder advisory votes on executive compensation (“say on pay” votes), which the Dodd-Frank Act now makes mandatory for all publicly traded companies. The share of executive-compensation-related proposals in 2013 was three percentage points above the share witnessed in the earlier 2006–10 period, once say-on-pay shareholder proposals are factored out. Investors interested in compensation issues seem to be seeking new avenues to affect management pay, outside the advisory votes that are now standard.

Among more narrowly defined proposal subtypes, the most introduced class of shareholder proposal in 2013 involved corporate political spending or lobbying—20 percent of all proposals, up from only 10 percent of all proposals through the full 2006–13 period (see “Special Focus: Proposals Related to Political Spending or Lobbying”). The second-most introduced subtype of shareholder proposal sought to split a company’s chairman and CEO roles; these proposals constituted 13 percent of all shareholder proposals in 2013, up from 8 percent in the full eight-year period. A total of 12 percent of all 2013 proposals involved the environment, up from 10 percent across the broader period.

Conversely, only 7 percent of shareholder proposals in 2013 involved voting rules, versus 14 percent across the 2006-13 period. This decline is attributable to two main factors. First, the most common type of voting-rule proposal, requiring a majority vote to elect directors, is germane for a shrinking share of the Fortune 250, as more and more companies have adopted majority-voting standards in director elections. Second, a relatively common class of voting-rule proposal across the eight-year period, seeking “cumulative voting” in director elections, virtually vanished this year, with but one such proposal making a ballot (at Chevron, and receiving 27 percent of the vote). (A cumulative-voting rule would permit a shareholder to cast multiple votes per share for a single preferred director candidate, up to the total number of candidates standing for election.) The disappearance of cumulative-voting proposals is mostly explained by the absence of longtime corporate gadfly Evelyn Davis, historically the most frequent proponent of this idea, from the 2013 proxy season.

Conversely, only 7 percent of shareholder proposals in 2013 involved voting rules, versus 14 percent across the 2006-13 period. This decline is attributable to two main factors. First, the most common type of voting-rule proposal, requiring a majority vote to elect directors, is germane for a shrinking share of the Fortune 250, as more and more companies have adopted majority-voting standards in director elections. Second, a relatively common class of voting-rule proposal across the eight-year period, seeking “cumulative voting” in director elections, virtually vanished this year, with but one such proposal making a ballot (at Chevron, and receiving 27 percent of the vote). (A cumulative-voting rule would permit a shareholder to cast multiple votes per share for a single preferred director candidate, up to the total number of candidates standing for election.) The disappearance of cumulative-voting proposals is mostly explained by the absence of longtime corporate gadfly Evelyn Davis, historically the most frequent proponent of this idea, from the 2013 proxy season.

IV. 2013 Shareholder-Proposal Voting Results

Although more shareholder proposals were introduced at Fortune 250 companies in 2013 than in any year since 2010, investor support for the proposals introduced was the lowest in the 2006–13 period. Among the shareholder proposals coming to a vote at the 218 companies holding annual meetings by August 15, only 7 percent received shareholders’ majority support, down from 9 percent in 2012.51 The average shareholder proposal received the support of 26 percent of shareholders in 2013, down from 27 percent in 2012.

|

SPECIAL FOCUS: PROPOSALS RELATED TO POLITICAL SPENDING OR LOBBYING

|

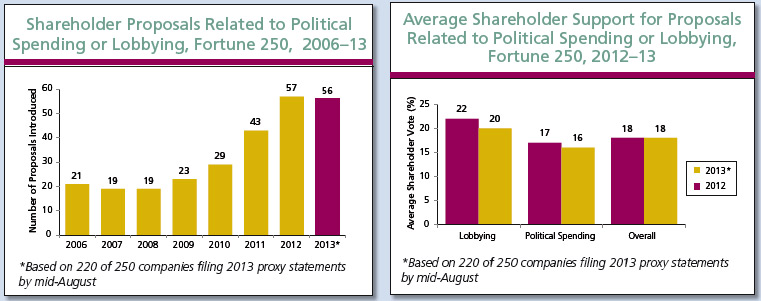

Fortune 250 companies have faced an increasing number of shareholder proposals related to a corporation's political spending or lobbying. From 2006 through 2009, the number of such proposals hovered between 19 and 23 proposals annually, but the number of these proposals has risen to 57 in 2012 and 56 (to date) in 2013;[44] proposals related to corporate political spending or lobbying have been more numerous than any other class of proposal in each of the last two years. One factor prompting this increase, at least according to the supporting statements of recent shareholder proposals relating to corporate political spending, is the Supreme Court's 2010 decision in Citizens United v. Federal Election Commission,[45] which determined that independent political expenditures were speech protected by the First Amendment to the United States Constitution, even as applied to corporations.[46]

Fortune 250 companies have faced an increasing number of shareholder proposals related to a corporation's political spending or lobbying. From 2006 through 2009, the number of such proposals hovered between 19 and 23 proposals annually, but the number of these proposals has risen to 57 in 2012 and 56 (to date) in 2013;[44] proposals related to corporate political spending or lobbying have been more numerous than any other class of proposal in each of the last two years. One factor prompting this increase, at least according to the supporting statements of recent shareholder proposals relating to corporate political spending, is the Supreme Court's 2010 decision in Citizens United v. Federal Election Commission,[45] which determined that independent political expenditures were speech protected by the First Amendment to the United States Constitution, even as applied to corporations.[46]

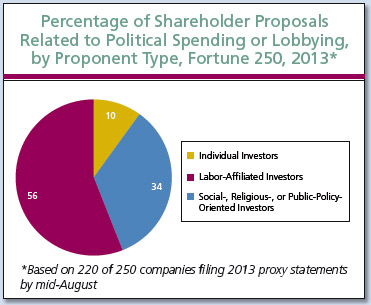

These proposals have largely been pushed by social-investing funds, religious-affiliated investing funds, and laboraffiliated investing funds, which together accounted for 90 percent of all political-spending-related proposals in 2013. Nine political-spending-related proposals in 2013 were sponsored by Catholic religious orders, and the New York State Common Retirement Fund, which holds assets in trust for the New York State & Local Retirement System (NYSLRS),[47] has sponsored eight, more than any other single investor. (The sole fiduciary of this fund is the state's elected comptroller, Democrat Thomas P. DiNapoli.[48] DiNapoli and the New York fund also filed suit in Delaware state court in 2013 against the Qualcomm company; DiNapoli sought access to certain of the company’s records related to political spending, but the case settled on February 22 after the company agreed to certain disclosures.)[49]

The composition of shareholder proposals related to political spending or lobbying shifted from 2012 to 2013. In 2012, two-thirds of all proposals in this class related to political spending but not lobbying; in 2013, 54 percent of all proposals involved lobbying. The decreased incidence in shareholder proposals related exclusively to political spending in 2013 is likely due in significant part to 2013, unlike 2012, not being a federal- or presidential-election year. Moreover, some shareholders may have been substantially satisfied by companies’ sharehold increased disclosure of political spending in response to previous years’ shareholder activism in this area.

Although shareholder proposals related to political spending or lobbying have been frequently introduced, they have failed to gain substantial traction with the broad class of investors. In both 2012 and 2013, proposals relating to political spending or lobbying received only 18 percent support, on average, from shareholders. Moreover, the shift in composition in shareholder proposals between 2012 and 2013 masks a subtle decrease in support for these proposals year over year, as proposals related to lobbying but not political spending have historically received marginally more support, on average, than those exclusively related to political spending. Shareholder support for lobbying-related proposals fell from 22 percent to 20 percent from 2012 to 2013, and support for proposals relating exclusively to political spending fell from 17 percent to 16 percent.[50]

|

In total, 20 shareholder proposals have received majority support from shareholder proposals in 2013:

- Seven seeking majority-voting requirements for director elections (of 12 introduced and coming to a vote);

- Six seeking to declassify the company’s board (of seven introduced and coming to a vote);

- Two seeking “proxy access,” the right for owners of a certain percentage of a company’s stock to nominate directors on the company’s proxy ballot (of six introduced and coming to a vote);

- Two seeking to separate the company’s chairman and CEO positions (of 34 introduced and coming to a vote);

- One seeking to permit shareholders holding a certain percentage of the company’s shares to call a special meeting, outside the annual meeting process (of seven introduced and coming to a vote);

- One seeking to permit shareholders to act outside annual meetings by written consent (of 18 introduced and coming to a vote); and

- One seeking a compensation clawback policy at medical supplier McKesson Corporation.[52]

As these results suggest, only a select few classes of shareholder proposal receive broad shareholder backing: 13 of 20 such proposals receiving majority support in 2013 called for either declassifying boards of directors or electing directors by simple majorities. The decreased incidence of such relatively “popular” proposals—in part a function of such rules being adopted as norms in an increasing percentage of America’s largest public companies—helps to explain the decline in the percentage of shareholder proposals winning majority support this year. In addition, the relatively robust stock market performance probably made many shareholders less likely to support changes to existing corporate-governance and executive-compensation arrangements.

Executive Compensation Advisory Votes

The results for Dodd-Frank-mandated executive-compensation advisory votes in 2013 closely mirrored those in 2012. Among the 204 Fortune 250 companies holding such votes by mid-August 2013, shareholder support for management pay averaged 88.5 percent, up marginally from 88.0 percent among the 232 such companies holding votes last year. In 2013, only four companies failed to receive majority support (Apache, Freeport-McMoRan, McKesson, and Navistar International), as compared to five in 2012 (Best Buy, Citigroup, Chesapeake Energy, Community Health Systems, and Oracle). Apache narrowly missed majority support for its pay package, with 49.82 percent of the vote, after the proxy advisory firm Institutional Shareholder Services (ISS) recommended a vote against the Apache executive-compensation package, to which the company objected on the grounds that ISS’s peer-group selection was inappropriate.53 Freeport-McMoran, McKesson, and Navistar each received below 30 percent shareholder support, the first two under pressure from labor-affiliated investors and the third under pressure from activist investor Carl Icahn.

V. Conclusion

The 2013 proxy season shows shareholder activism in the form of shareholder proposals submitted for consideration on corporate proxy ballots on the rise. Such proposals, however, received less support this year than in any of the prior seven years in the Proxy Monitor database.

Despite scant voting support, shareholder proposals are likely here to stay. Sponsors of shareholder proposals can impose significant costs on corporate management regardless of whether their proposals pass—as evidenced by companies regularly going to the time and expense to file formal submissions to the SEC permitting them to exclude shareholder proposals from the ballot. Apart from the direct cost of responding to such proposals, certain types of shareholder proposals may be sensitive to many companies leery of offending their customer base—which probably explains why a plurality of all shareholder proposals in 2012 and 2013 have related to corporate political spending or lobbying, notwithstanding limited support for such proposals.

Thus, shareholder activists interested in objectives other than share-price maximization can use the shareholder proposal process as leverage over management to achieve their objectives. Such shareholders may in fact dominate this process. Only one percent of shareholder proposals, in 2013 and across the 2006–13 period, have been sponsored by institutional investors without a tie to organized labor or with an express social-investing, religious, or public-policy purpose. Labor-affiliated investors, which sponsored a plurality of all shareholder proposals in 2013, sponsored them more often at companies that play a larger role in the political process and that contribute more heavily in support of the Republican Party.

In sum, the evidence suggests that the shareholder proposal process serves largely to empower shareholders with objectives unrelated to share value and quite possibly against the interests of the broader class of diversified holders of equity securities. Although each of the hypotheses tested herein warrants further study, the findings of this report, in conjunction with other reports and findings published over the last three years that analyze data in the Proxy Monitor database, throw into question the degree to which the shareholder proposal process as currently structured is consistent with the SEC’s mandate to promote efficiency, competition, and capital formation.

ENDNOTES

- Stockholders of publicly traded companies who have held shares valued at $2,000 or more for at least one year can introduce proposals for shareholders’ consideration at corporate annual meetings. See 17 C.F.R. § 240.14a-8 (2007) [hereinafter 14a-8]. The federal Securities and Exchange Commission determines the procedural appropriateness of a shareholder proposal for inclusion on a corporation’s proxy ballot, pursuant to the Securities Exchange Act of 1934, Pub. L. No. 73-291, Ch. 404, 48 Stat. 881 (1934) (codified at 15 U.S.C. §§ 78a–78oo (2006 & Supp. II 2009)), at §§ 78m, 78n & 78u; 15 U.S.C. §§ 80a-1 to 80a-64 (2000) (pursuant to, Investment Company Act of 1940, Pub. L. No. 76-768, 54 Stat. 841(1940)); but the substantive rights governing such measures and how they can force boards to act remain largely a question of state corporate law, cf. Del. Code Ann., tit. 8, § 211(b) (2009) (noting that in addition to the election of directors, “any other proper business may be transacted at the annual meeting”).

- Under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, publicly traded companies must hold shareholder advisory votes on executive compensation annually, biennially, or triennially, at shareholders’ discretion. See Pub. L. No. 111-203, 124 Stat. 1376, §951 (2010) [hereinafter Dodd-Frank Act].

- The ProxyMonitor.org database includes the 250 largest publicly traded American companies, by revenues, as determined by Fortune magazine (the “Fortune 250”).

- See Proxy Monitor, Reports and Findings, http://proxymonitor.org/Forms/reports_findings.aspx (last visited Aug. 11, 2013).

- See 14a-8, supra note 1.

- See James R. Copland et al., Proxy Monitor 2012: A Report on Corporate Governance and Shareholder Activism, 6 (Manhattan Inst. for Pol’y Res., Fall 2012); Copland, Proxy Monitor 2011: A Report on Corporate Governance and Shareholder Activism, 7 (Manhattan Inst. for Pol’y Res., Fall 2011).

- See JPMorgan Chase & Co, Definitive Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934, proposal 6 (2013), http://www.sec.gov/Archives/edgar/data/19617/000001961713000255/jpmc2013definitiveproxysta.htm#s5F565B3CE6189A603874A810F3791135; see also Dan Fitzpatrick et al., Vote Strengthens Dimon’s Grip: J.P. Morgan Shareholders Reject Proposal to Divide Top Posts; Board Under Fire, WALL ST. J. (May 21, 2013), available at http://online.wsj.com/article/SB10001424127887324787004578496814286493352.html.

- See Copland, Eliot Spitzer’s great big (bad) idea, N.Y. POST (July 26, 2013), available at http://www.nypost.com/p/news/opinion/opedcolumnists/eliot_spitzer_great_big_bad_idea_XR3A8FIvZShwalLJDjoLXI; see also Isaac Gorodetski, Manhattan Moment: Eliot Spitzer looking to steamroll corporate boards at the expense of city workers?, WASH. EXAMINER (July 11, 2013), available at http://washingtonexaminer.com/eliot-spitzer-looking-to-steamroll-corporate-boards-at-the-expense-of-city-workers/article/2532965.

- See Dodd-Frank Act, supra note 2.

- See id.

- See No-Action Letters, U.S. Securities and Exchange Commission, http://www.sec.gov/answers/noaction.htm (last visited Aug. 20, 2013).

- See id.

- As discussed in the 2013 Winter Report, Copland, Political Spending, Say on Pay, and Other Key Issues to Watch in the 2013 Proxy Season (Manhattan Inst. for Pol’y Res., Winter 2013), a survey conducted through the Society of Corporate Secretaries and Governance Professionals, see Society of Corporate Secretaries and Governance Professionals, http://www.ascs.org (last visited Feb. 27, 2013), of the society’s member companies in the ProxyMonitor.org database, showed that companies faced on average 2.15 shareholder proposals overall in 2012. Although this survey may not present an unbiased picture of shareholder-proposal activity, for reasons discussed in that report, its finding, in conjunction with published SEC no-action filings, suggests that among the shareholder proposals introduced to Fortune 250 companies but not placed on proxy ballots roughly 51 percent were withdrawn by shareholders after some negotiation with the company and 49 percent were excluded by the company after receiving an SEC no action letter.

- See 14a-8, supra note 1.

- See id.

- For a fuller discussion of Chevedden and Steiner and their shareholder activism historically, see 2012 Report, supra note 6.

- “Corporate Gadflies” as commonly used in Charles M. Yablon, Overcompensating: The Corporate Lawyer and Executive Pay, 92 COLUM. L. REV. 1867, 1895 (1992); Jessica Holzer, Firms Try New Tack against Gadflies, WALL. ST. J. (Jun. 6, 2011), http://online.wsj.com/article/SB10001424052702304906004576367133865305262.html.

- New York City’s elected comptroller—currently Democrat John Liu—is one of several trustees, spread across independent boards overseeing five different pensions with a collective $130 billion in assets. See New York City Comptroller John C. Liu, Pension Funds, Overview of the NYC Public Pension Funds, http://comptroller.nyc.gov/general-information/pension-funds-asset-allocation/ (last visited Aug. 20, 2013). Board members tend to be political officials or union delegates: the board of the $46 billion Teachers Retirement System (TRS) includes the comptroller, two mayoral delegates, a delegate from the education chancellor, and three teacher delegates, see Teachers’ Retirement System of the City of New York, Our Retirement Board, https://www.trsnyc.org/trsweb/aboutUs/ourRetirementBoard.html (last visited Aug. 20, 2013); whereas the board of the $43 billion New York City Employees’ Retirement System (NYCERS) includes the comptroller, the public advocate, a mayoral representative, each of the five New York City borough presidents, and three union delegates, see NYC Employees’ Retirement System, Board of Trustees, http://www.nycers.org/%28S%284wrsjxi1mhx2ru45mnycd445%29%29/about/Board.aspx (last visited Aug. 20, 2013).

In contrast to New York City’s pension structure, the sole trustee of the $160 billion New York State Common Retirement Fund is the elected state comptroller, currently Democrat Thomas P. DiNapoli. See Office of the State Comptroller, Fiduciary Responsibilities of the Comptroller, http://www.osc.state.ny.us/pension/fiduciary.htm (last visited Aug. 20, 2013); see also Press Release, The Office of the New York State Comptroller Thomas P. DiNapoli, DiNapoli: State Pension Fund Valued At All-Time High Of $160.4 Billion (May 13, 2013), http://www.osc.state.ny.us/press/releases/may13/051313.htm. For a fuller discussion of the structure and shareholder activism of the New York City and State pension funds, as well as other state and municipal pension funds, see Copland, Public Pension Fund Activism: Public-employee pension funds, led by New York City and State, assume a leading role in sponsoring shareholder proposals (Manhattan Inst. for Pol’y Res., Finding 3, 2013), http://proxymonitor.org/Forms/2013Finding4.aspx.

- Copland, Proxy Monitor 2011, supra note 6, at 16–18.

- Copland, 2013 Proxy Season Wrapping Up: More shareholder proposals have been introduced this year, but their success rate is down (Manhattan Inst. for Pol’y Res., Finding 4, 2013),

http://proxymonitor.org/Forms/2013Finding4.aspx.

- For a fuller discussion of such activism, see Finding 3, supra note 18.

- For a fuller discussion of the distinctions among private labor-affiliated pension fund activism, see Finding 4, supra note 20.

- See Copland, Proxy Monitor 2012, supra note 6, at 16-17; see also Copland, Proxy Monitor 2011, supra note 6, at 10-11; see also Copland, Season-End Report: Evidence suggests union-fund shareholder activism related to objectives other than share price (Manhattan Inst. for Pol’y Res., 2012), http://proxymonitor.org/Forms/2012Finding4.aspx.

- Pub. L. No. 93-406, § 514, 88 Stat. 829, 897 (1974) (codified at 29 U.S.C. §§ 1001-1461 (2006)).

- 29 C.F.R. § 2509.08-2(1) (2008).

- See 29 U.S.C. § 1003(b).

- Based on data submitted to the Federal Election Commission and published by the Center for Responsive Politics (compiled by Manhattan Institute researchers, on file with author). That every single Fortune 250 company gave money to politics in 2012 undercuts seriously claims that playing any active role in politics hurts share value. Compare John C. Coates IV, Corporate Politics, Governance, and Value Before and After Citizens United, 9 J. EMPIRICAL LEGAL STUD. 657, 680–90 (2012) (showing empirical results showing that political participation hurts shareholder value) with Robert J. Shapiro & Douglas Dowson, Corporate Political Spending: Why the New Critics Are Wrong, in Legal Pol’y Rep. 15, (Manhattan Inst. for Pol’y Res. June 2012), http://www.manhattan-institute.org/html/lpr_15.htm (showing Coates’s results to differ from most studies on the subject and criticizing Coates’s methodology). In a letter to the SEC, Professor Coates has attacked Shapiro and Dowson’s characterization of his work, see Letter from John C. Coates IV, to Elizabeth M. Murphy, Sec’y, U.S. Sec. & Exch. Comm’n, at 1 (Feb. 4, 2013), available at http://www.sec.gov/comments/4-637/4637-1473.pdf, to which the principal author of this report has responded, see Copland, Against an SEC-Mandated Rule on Political Spending Disclosure: A Reply to Bebchuk and Jackson, 9 Harv. Bus. L. Rev. 901, n.54 (2013) (forthcoming).

- Based on data submitted to the Federal Election Commission and published by the Center for Responsive Politics (compiled by Manhattan Institute researchers, on file with author).

- Id.

- Id.

- See Copland, Proxy Monitor 2012, supra note 6, at 16–17

- Kristen Schorsch, Abbott, AbbVie seek investors’ love, CRAIN’S CHI. BUS. (Apr. 30, 2013), http://www.chicagobusiness.com/article/20130430/NEWS03/130439983/abbott-abbvie-seek-investors-love.

- This report’s primary author, James R. Copland, owns shares in several of the companies mentioned here as part of a diversified equity portfolio, including Chevron, Eli Lilly, ExxonMobil, Merck, Pfizer, and Royal Dutch Shell.

- Copland, Proxy Monitor 2012, supra note 6, at 17 (citing Edward McClelland, Basic Union Busting, NBC CHICAGO, Oct. 13, 2011, http://www.nbcchicago.com/blogs/ward-room/Basic-Union-Busting-131252434.html).

- Dean Foods, 2012 Annual Report, Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934: For The Fiscal Year Ended December 31, 2012, http://www.deanfoods.com/media/64164/annualreport_2012.pdf.

- See Copland, Proxy Monitor 2012, supra note 6, at 17 (citing Alison Fitzgerald, Dean Foods Accused as Dairy Farmers Say They Are Getting Milked, PPJ GAZETTE, May 28, 2010, http://ppjg.me/2010/05/28/dean-foods-accused-as-dairy-farmers-say-they-are-getting-milked/).

- Open Secrets, Exxon Mobil: Total Contributions, http://www.opensecrets.org/orgs/totals.php?id=D000000129&cycle=2012 (last visited Aug. 20, 2013).

- Derek Hoffman, CenturyLink Earnings: Here’s Why Investors are Selling Shares Now, WALL ST. CHEAT SHEET BLOG (Feb. 13, 2013),

http://wallstcheatsheet.com/stocks/centurylink-earnings-heres-why-investors-are-selling-shares-now.html/?a=viewall.

- This report’s primary author, James R. Copland, owns shares in AT&T, CenturyLink, and Verizon as part of a diversified equity portfolio.

- See Yayat Supriatna & Michael Taylor, Freeport Indonesia union threatens walkout from Friday, REUTERS (June 13, 2013, 2:51 AM),

http://www.cnbc.com/id/100812089.

- See Press Release, CenturyLink, CenturyLink and CWA reach agreement in contract negotiations (June 30, 2013), http://news.centurylink.com/index.php?s=43&item=3067.

- See Nick Jonson, Talks between Freeport-McMoRan, Indonesian government continuing: CEO, PLATTS, (Apr. 18, 2013, 1:20 PM), http://www.platts.com/latest-news/metals/Washington/Talks-between-Freeport-McMoRan-Indonesian-government-21964187.

- See Supriatna & Taylor, supra note 40.

- Given that 30 companies have yet to file proxy documents as of this writing, the 56 political-spending-related proposals introduced thus far in 2013 represent a 12 percent increase year-over-year to the 57 introduced for all 250 companies in 2012.

- 130 S. Ct. 876 (2010).

- See 3M Company, Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934, proposal no. 5 (Mar. 27, 2013), available at http://www.sec.gov/Archives/edgar/data/66740/000104746913003491/a2213428zdef14a.htm#Proposal_5.

- See Office of the State Comptroller, New York State and Local Retirement System, http://www.osc.state.ny.us/retire/index.php (last visited Aug. 20, 2013); Office of the State Comptroller, Snapshot of the New York State Common Retirement Fund, http://www.osc.state.ny.us/pension/snapshot.htm (last visited Aug. 20, 2013).

- See Office of the State Comptroller, Fiduciary Responsibilities of the Comptroller, supra note 18.

- See Dan Strumpf, Qualcomm Settles Disclosure Suit with New York, WALL ST. J. (Feb. 22, 2013), available at http://online.wsj.com/article/SB10001424127887323549204578320500077425818.html.

50 For these and other purposes, the Manhattan Institute counts shareholder support consistent with the practice dictated in a company’s bylaws, consistent with state law. Some companies measure shareholder support by dividing the number of votes For a proposal by the total number of shares present and voting (For and Against), ignoring abstentions. Other companies measure shareholder support by dividing the number of favorable votes by the number of shares present and entitled to vote—effectively counting abstentions as Against votes.

Certain shareholder activists in this arena argue that support for shareholder proposals should be counted solely in the former matter. Among these is the Center for Political Accountability (CPA), an advocacy group headed by former Democratic congressional staffer Bruce Freed that claims as its objective “to bring transparency and accountability to corporate political spending” and which promulgates a “model shareholder resolution” for shareholder activists to introduce in the proxy process. See Center for Political Accountability, About the CPA, http://www.politicalaccountability.net/index.php?ht=d/sp/i/870/pid/870/pid/190; Political Disclosure and Oversight Resolution 2013, http://www.politicalaccountability.net/index.php?ht=d/sp/i/867/pid/867 (last visited Aug 20, 2013). CPA claims that it “follows the SEC method of counting shareholder votes, which uses only the numbers of shares voted in favor and against a resolution.” Center for Political Accountability, Reality Check on Arguments against Corporate Political Accountability and Disclosure, at 2 (May 8, 2013), available at http://www.politicalaccountability.net/index.php?ht=a/GetDocumentAction/i/7828.

The CPA’s claim is deceptive. It is true that the SEC, for the purposes of determining whether a proposal has met the “resubmission threshold” to qualify for inclusion on a corporate ballot, has determined that “[o]nly votes for and against a proposal are included in the calculation of the shareholder vote of that proposal,” ignoring abstentions. SEC Staff Legal Bulletin No. 14, F.4., July 13, 2001, available at http://www.sec.gov/interps/legal/cfslb14.htm (last visited August 16, 2013). (There are many reasons why the SEC might choose to follow a single ballot-counting standard in determining whether a company can exclude a shareholder proposal previously submitted that failed to garner a minimum 3 percent, 6 percent, or 10 percent vote as required to be reintroduced in subsequent years, see Amendments to Rules on Shareholder Proposals, Exchange Act Release No. 40,018; 63 Fed. Reg. 29,106, 29,108 (May 28, 1998) (codified at 17 C.F.R. pt. 240), http://www.sec.gov/rules/final/34-40018.htm#foot9 (“If the proposal deals with substantially the same subject matter as another proposal or proposals that has or have been previously included in the company’s proxy materials within the preceding 5 calendar years, a company may exclude it from its proxy materials for any meeting held within 3 calendar years of the last time it was included if the proposal received: (i) Less than 3% of the vote if proposed once within the preceding 5 calendar years; (ii) Less than 6% of the vote on its last submission to shareholders if proposed twice previously within the preceding 5 calendar years; or(iii) Less than 10% of the vote on its last submission to shareholders if proposed three times or more previously within the preceding 5 calendar years.”)—including reducing workload in processing 14a-8 no-action petitions and adopting a permissive standard for ballot inclusion, given shareholders’ ability to reject proposals previously voted down by large margins.)

Whatever the merits of the SEC’s counting methodology in the procedural resubmission context, state law clearly governs the appropriate method by which a corporation counts votes in assessing its own ballot items, consistent with the longstanding general principle under federal securities law that substantive corporate-governance issues are a question of state law. That state law and corporate bylaws govern proxy ballot voting is clearly implied in the SEC’s Schedule 14A, which specifies the information required for inclusion in proxy statements and which asks companies to “[d]isclose the method by which votes will be counted, including the treatment and effect of abstentions and broker non-votes under applicable state law as well as registrant charter and by-law provisions,” for “each matter which is to be submitted to a vote of security holders.” Schedule 14A, Item 21. Voting Procedures, available at http://taft.law.uc.edu/CCL/34ActRls/rule14a-101.html (last visited August 16, 2013).

The state law of Delaware, in which most large public corporations are chartered, is clear that “the certificate of incorporation or bylaws of any corporation authorized to issue stock may specify the number of shares and/or the amount of other securities having voting power the holders of which shall be present or represented by proxy at any meeting in order to constitute a quorum for, and the votes that shall be necessary for, the transaction of any business.” Del. Gen. Corp. L. § 216. And indeed the default rule under Delaware law, absent a bylaw specification, is “in all matters other than the election of directors,” to count “the affirmative vote of the majority of shares of such class or series or classes or series present in person or represented by proxy at the meeting,” id. at 216(4)—the very bylaw voting specification rejected by the CPA and certain other social-investing activists. Though it is understandable that the sponsors of and advocates for various shareholder proposals might wish to maximize the voting results they report for the proposals they support, there is no justification, in the authors’ view, for counting shareholder votes on shareholder proposals contrary to the manner specified in corporate bylaws and under state law.

- In determining whether a shareholder proposal receives majority support from shareholders, and otherwise tabulating votes on shareholder proposals, the Manhattan Institute follows voting methodologies in company bylaws, consistent with state law. See id. (discussing rationale). To determine the percentage of proposals receiving majority support and the average percentage vote on shareholder proposals, the Manhattan Institute counts only those proposals actually coming to a vote, omitting proposals withdrawn in advance of the annual meeting.

- Voting percentages do not correspond exactly to those shown in the graph, “Percentage of Shareholder Proposal Subtypes Receiving Majority Support,” given that “voting rules” includes proposals other than those seeking to elect directors by a simple majority voting standard and “special meetings/written consent” aggregates those two proposal classes.

- Half of the companies that ISS selected as Apache’s peers were not, like Apache, in the oil and gas sector, and many of them had a significantly smaller market capitalization, as little as 10 percent of Apache’s size. See Apache Corporation, Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934, Definitive Additional Materials (May 1, 2013), available at http://www.sec.gov/Archives/edgar/data/6769/000119312513192941/d528930ddefa14a.htm.