Manhattan Institute Proxy Monitor Finding 7

2011 Proxy Season Review

Database Reveals Decline in Successful Shareholder Proposals

Share of Proposals Concerning Social Policy Increase

Download PDF

As of this writing, 84 of the Fortune 100 companies in the Manhattan Institute’s ProxyMonitor.org database have held their 2011 annual meetings, with four more scheduled to meet by the end of June. With so many companies completing their annual proxy voting, we can draw some conclusions about overall shareholder proposal activity relative to prior years.

The total number of shareholder proposals introduced per company in 2011 was lower than in any of the prior three years and the percentage of shareholder proposals adopted fell to the lowest level since 2008. However, the number of proposals related to social policy (i.e., unrelated to corporate governance or executive compensation) reached historic highs, driven by an increasing number of proposals devoted to corporations’ political spending. Although no social policy proposal has passed over the past four years, the number of such proposals garnering support from at least 30 percent of shareholders is on the rise. This trend merits ongoing attention. Analysis of future social policy proposals should focus particularly on the subset of such proposals in the political-spending arena.

Overall Shareholder Proposal Trends

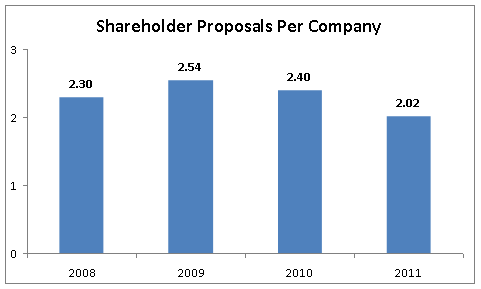

As shown in the graph on the right, the average number of shareholder proposals introduced at Fortune 100 companies fell by 16 percent in 2011, with only 2.02 shareholder proposals per company. This decline, however, is largely attributable to a sharp drop-off in the number of shareholder proposals devoted to executive compensation—a direct function of “say on pay” shareholder votes now being required under Section 951 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The effect of this new requirement has been to eliminate what had been one of the most popular shareholder proposals. As shown below, through June, only 12 percent of all shareholder proposals in 2011 involved executive compensation—down from 30 percent over the 2008-2010 period.

As shown in the graph on the right, the average number of shareholder proposals introduced at Fortune 100 companies fell by 16 percent in 2011, with only 2.02 shareholder proposals per company. This decline, however, is largely attributable to a sharp drop-off in the number of shareholder proposals devoted to executive compensation—a direct function of “say on pay” shareholder votes now being required under Section 951 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The effect of this new requirement has been to eliminate what had been one of the most popular shareholder proposals. As shown below, through June, only 12 percent of all shareholder proposals in 2011 involved executive compensation—down from 30 percent over the 2008-2010 period.

In 2011, the number of shareholder proposals related to corporate governance also fell, on a per-company basis, to 12 percent below 2010 levels and 8 percent below the 2008-2010 average. In part, this decrease is attributable to past successes among shareholder proposals in this category, as the proposals most likely to be adopted have already been embraced by many Fortune 100 companies. These include: proposals requiring a majority of shareholder support for director elections; proposals declassifying boards to require annual director elections; and proposals authorizing shareholders to act outside of annual meetings by written consent or by calling special meetings.

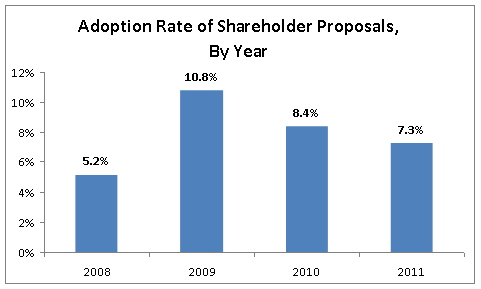

Past successes, as well as the absence of the previously popular “say on pay” proposals, also help to explain the drop in overall adoption rates for shareholder proposals generally. As the graph

below shows, the adoption rate for shareholder proposals in 2011 continued to decline from its 2009 high, with only 7.3 percent of all shareholder proposals receiving the support of a majority of shares voted—a decline of almost 14 percent from 2010.

Past successes, as well as the absence of the previously popular “say on pay” proposals, also help to explain the drop in overall adoption rates for shareholder proposals generally. As the graph

below shows, the adoption rate for shareholder proposals in 2011 continued to decline from its 2009 high, with only 7.3 percent of all shareholder proposals receiving the support of a majority of shares voted—a decline of almost 14 percent from 2010.

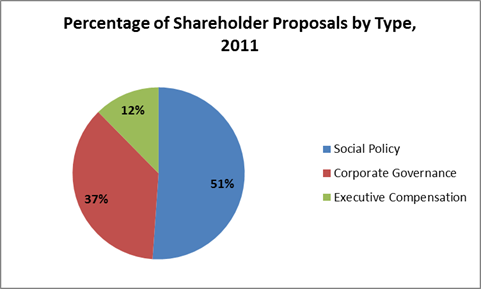

In addition to the change in composition of the pool of proposals related to executive compensation and corporate governance, the increase in proposals related to social policy also helps to explain the 2011 fall in the shareholder-proposal adoption rate. As shown in the earlier graph, social policy proposals in 2011 constituted 51 percent of all shareholder proposals introduced. This represents a substantial increase from the 2008-2010 period, in which such proposals constituted, on average, 38 percent of all proposals introduced. Since no social policy proposal introduced at a Fortune 100 company since 2008 has been adopted, the share of shareholder proposals devoted to social policy substantially affects the average overall adoption rate; indeed, the increased share of 2011 proposals devoted to social policy, on its own, wholly accounts for the drop in shareholder-proposal passage relative to 2010. An analysis of shareholder votes which controlled for type could reveal that there has been increased pressure on boards, notwithstanding the summary-statistic decline.

Focus on Social Policy Proposals: Political Spending

Focus on Social Policy Proposals: Political Spending

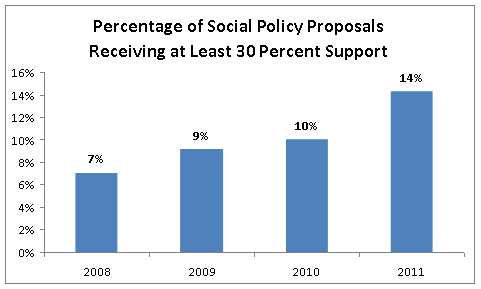

In 2011, the number of shareholder proposals related to social policy grew in both relative and absolute terms; at 1.03, the number of social-policy proposals introduced per company was 16 percent more than in 2010 and 18 percent above the 2008-2010 average. Although no social policy proposals received a majority of shareholder support in 2011—consistent with the 2008-2010 period—the share of such proposals garnering the support of at least 30 percent of shareholders continued to rise, as shown in the graph

below.

Driving both the increase in social-policy proposals and the sizable (if non-majority) shareholder support for such proposals was an increase in the number of proposals related to political spending—a trend we predicted in Finding 2.[1] In 2011, 32 percent of all social policy proposals have related to corporate political spending. This is a sharp increase from 2008-2010, when political spending was the topic of only 19 percent of proposals related to social policy. And nine of the 13 social policy proposals that received the support of at least 30 percent of shareholders in 2011 related to corporations’ political spending.

The increasing shareholder interest in corporations’ political spending is likely due in significant part to the Supreme Court’s controversial 2010 decision in Citizens United v. Federal Election Commission,[2] holding that corporate political expenditures are speech protected by the First Amendment. Certain voices in both the academic and investment community—such as Harvard’s Lucian Bebchuk, Columbia’s Robert Jackson, and Vanguard founder John Bogle—have called for a greater shareholder say over corporate political speech.[3] Other leading voices, including Illinois’s Larry Ribstein and UCLA’s Stephen Bainbridge, have questioned the appropriateness of the shareholder proxy process for handling such questions;[4] Professor Ribstein has expressed concern that “shareholder voting on corporate speech could amplify activist business skeptics while muting the diversified shareholders who would prefer that business views be heard” and worried that “[t]he most likely effect (and possible intent) of requiring shareholder voting on corporate contributions would be to burden and therefore reduce corporations’ ability to speak at all.”[5]

The increasing shareholder interest in corporations’ political spending is likely due in significant part to the Supreme Court’s controversial 2010 decision in Citizens United v. Federal Election Commission,[2] holding that corporate political expenditures are speech protected by the First Amendment. Certain voices in both the academic and investment community—such as Harvard’s Lucian Bebchuk, Columbia’s Robert Jackson, and Vanguard founder John Bogle—have called for a greater shareholder say over corporate political speech.[3] Other leading voices, including Illinois’s Larry Ribstein and UCLA’s Stephen Bainbridge, have questioned the appropriateness of the shareholder proxy process for handling such questions;[4] Professor Ribstein has expressed concern that “shareholder voting on corporate speech could amplify activist business skeptics while muting the diversified shareholders who would prefer that business views be heard” and worried that “[t]he most likely effect (and possible intent) of requiring shareholder voting on corporate contributions would be to burden and therefore reduce corporations’ ability to speak at all.”[5]

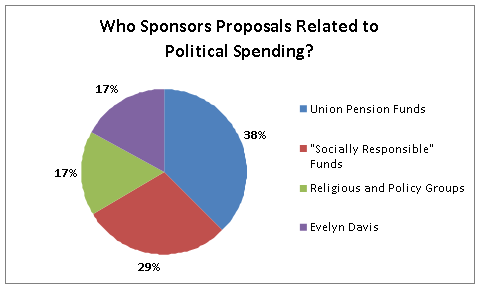

Data from the Proxy Monitor database offer at least some support for Professor Ribstein’s concern that shareholder proposals involving political speech might be advancing the interests of “activist business skeptics” at the expense of ordinary diversified shareholders.[6] As shown in the graph on the right, a plurality of all such proposals were backed by labor union pension funds, with the bulk of the remainder being sponsored by “socially responsible” investment funds and religious and policy groups, each of which has at least some potential political interest separate from share-price maximization.[7] These factors warrant further study, particularly if the number of shareholder proposals continues to increase, and especially if such proposals begin to garner more shareholder support than they have to date.

Data from the Proxy Monitor database offer at least some support for Professor Ribstein’s concern that shareholder proposals involving political speech might be advancing the interests of “activist business skeptics” at the expense of ordinary diversified shareholders.[6] As shown in the graph on the right, a plurality of all such proposals were backed by labor union pension funds, with the bulk of the remainder being sponsored by “socially responsible” investment funds and religious and policy groups, each of which has at least some potential political interest separate from share-price maximization.[7] These factors warrant further study, particularly if the number of shareholder proposals continues to increase, and especially if such proposals begin to garner more shareholder support than they have to date.

This report analyzes information gathered from the Manhattan Institute’s ProxyMonitor.org database, which contains information relating to all shareholder proposals submitted for shareholder vote since 2008, for the 100 largest American public companies.

ENDNOTES

- See Manhattan Institute Proxy Monitor Finding 2 (2011), available at http://www.proxymonitor.org/Forms/Finding2.aspx.

- 130 S. Ct. 876.

- See, e.g., Lucian A. Bebchuk & Robert J. Jackson, Jr., Corporate Political Speech: Who Decides?, 124 Harv. L. Rev. 83 (2010), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1670085;John C. Bogle, The Supreme Court Had Its Say. Now Let Shareholders Decide., NY Times, May 14, 2011, at WK9, available at http://www.nytimes.com/2011/05/15/opinion/15bogle.html.

- See, e.g., Larry Ribstein, The First Amendment and Corporate Governance, TruthontheMarket.com, May 24, 2011, http://truthonthemarket.com/2011/05/24/the-first-amendment-and-corporate-governance-2/; see also Stephen Bainbridge, Shareholders and Corporate Political Speech, ProfessorBainbridge.com, May 23, 2011, http://www.professorbainbridge.com/professorbainbridgecom/2011/05/shareholders-and-corporate-political-speech.html. Also see Professor Ribstein’s more extended academic paper on the topic, The First Amendment and Corporate Governance(2010), available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1739264.

- The First Amendment and Corporate Governance, http://truthonthemarket.com/2011/05/24/the-first-amendment-and-corporate-governance-2/.

- See also generally Roberta Romano, Less Is More: Making Shareholder Activism a Valued Mechanism of Corporate Governance, 18 Yale J. Reg. 174, 231-32 (2001) (“It is quite probable that private benefits accrue to some investors from sponsoring at least some shareholder proposals. The disparity in identity of sponsors—the predominance of public and union funds, which, in contrast to private sector funds, are not in competition for investor dollars—is strongly suggestive of their presence.”).

- On the potential conflict of interest facing labor union pension funds in shareholder proposal sponsorship and voting, see See Manhattan Institute Proxy Monitor Finding 6 (2011), available at http://www.proxymonitor.org/Forms/Finding6.aspx; see also the report cited therein by the Office of the Inspector General of the Department of Labor, available at http://www.governanceprofessionals.org/society/Department_Of_Labor_Office_of_Inspector_General_Is.asp?SnID=2.